Starting January 1, 2026, the U.S. tax code changes charitable giving in ways that matter for almost everyone:

- Individuals who take the standard deduction can now get a permanent, pre-tax (above-the-line) charitable deduction.

- Employers face new incentives to structure workplace giving and matching programs more intentionally.

- Finance teams now have clearer thresholds to model when corporate giving is deductible and when it isn’t.

- Nonprofits should expect donors to ask new questions and shift toward simpler, more trackable giving patterns (especially workplace giving).

This longread is the “one page” you can send to an employee, an HR leader, a CFO, or a nonprofit partner to explain what’s changing, what stays the same, and what to do next. It is designed to be understandable end-to-end without reading anything else — and it links to deeper guides if you want to go further.

Executive Summary: Who This Is For and Why It Matters

This guide is for four groups:

Individual and employee donors

You can now deduct up to $1,000 (single filers) or $2,000 (married filing jointly) in qualified charitable donations even if you take the standard deduction. That means charitable giving can reduce your taxable income without itemizing.

HR and CSR leaders

You have a rare opportunity: a real policy change that makes giving easier to promote because it is both meaningful and financially rational. If you communicate it well and align your program design, you can improve participation and employee engagement.

CFOs and Finance teams

Corporate giving rules now introduce thresholds that can make scattered giving less tax-efficient and structured giving more predictable. That changes how you plan budgets, forecast taxable income, and document contributions.

Nonprofits

This is a moment to refresh donor messaging (especially for everyday donors) and strengthen workplace giving partnerships, because employees will have a clearer incentive to give — and employers will have reasons to make giving frictionless.

If you only read one thing: 2026 introduces a new, permanent charitable tax incentive for standard-deduction filers, and it creates a stronger business case for structured workplace giving programs.

A Plain-English Overview of the 2026 Charitable Giving Rules

There are two separate (but related) storylines in 2026:

1) Individuals: a permanent “universal” charitable deduction

In plain English: most people use the standard deduction, and historically that meant their charitable donations did not change their taxes. Starting in 2026, many taxpayers can still take the standard deduction and also deduct a limited amount of charitable giving above the line.

This is why people are calling it “universal”: it extends tax benefit access to the majority of households.

For a short version optimized around this specific topic, see: The New 2026 Universal Charitable Deduction in Plain English.

2) Employers: more incentive to structure giving

Employers need to think about two different “channels” of giving:

- Employee-funded giving (employees donate their own money; they may now get an above-the-line deduction up to the cap)

- Company-funded giving (matching gifts, corporate grants, Cause Credits/Dollars for Doers, disaster relief contributions, etc.)

In 2026, good program design can help employees make the most of the new rules and can help companies budget and report giving more efficiently.

For a quick employer overview, see: What CFOs Need to Know About Corporate Giving in 2026.

3) Nonprofits: donor behavior may shift

This change isn’t only about taxes — it’s about predictability.

When giving becomes easier to track and explain (especially through employer programs), nonprofits can expect:

- More recurring gifts

- More donors asking “does this qualify?”

- More giving tied to seasonal campaigns (Giving Tuesday, disaster response, heritage months)

A nonprofit-focused guide lives here: 2026 Charitable Giving Tax Rules: What Nonprofits Should Know.

Deep Dive: The Universal Charitable Deduction for Individuals

What the this new universal deduction for donations?

Starting in 2026, many standard-deduction filers can take a limited charitable deduction above the line — meaning it reduces taxable income before other deductions and calculations.

The practical takeaway: you don’t have to itemize to receive a tax benefit for giving (up to the cap).

How much you can deduct

- $1,000 for individuals (single filers)

- $2,000 for married couples filing jointly

If you give more than the cap, you still gave more (which is great), but this particular incentive applies to the first $1,000 / $2,000.

Eligibility: who counts as a “qualified” nonprofit

When people say “IRS-qualified nonprofit,” what they usually mean is a U.S. organization eligible to receive tax-deductible charitable contributions — typically a registered 501(c)(3) public charity (and certain other qualifying entities). Employees shouldn’t have to become tax experts to donate correctly. They just need confidence that the organization they’re supporting is eligible.

This is one reason employer giving programs matter: platforms can handle verification centrally. Percent Pledge does this through built-in charity vetting inside the Giving Platform, so employees can donate with confidence.

What types of donations qualify (and what doesn’t)

Typically qualifies

- Cash donations (credit card, ACH, payroll giving) to eligible tax-deductible organizations

- Donations made during the calendar year 2026 and later

- Employee donations made through an employer giving program (your donation is still your donation)

Typically does not qualify for this specific incentive

- Contributions to donor-advised funds (DAFs)

- Non-cash donations (like clothing or household items) for purposes of this specific above-the-line deduction

- Value received in return (like event tickets where you got a benefit; only the charitable portion may count)

One point that confuses employees: company matching funds. The company’s match is a separate corporate donation. It does not increase the employee’s personal deduction — but it absolutely increases the total impact. That’s why matching is so powerful, especially when paired with the new personal deduction incentive. (More on this in the employer section.)

Another important point is clarifying Donor-Advised Funds (DAFs), which are becoming an increasingly popular way to give back. Here are two quick FAQs on the DAF topic:

Why are DAF contributions excluded?

A donor-advised fund (DAF) is treated as a charitable giving vehicle where the donor makes a contribution to the DAF (which is a public charity sponsor) and then later recommends grants to operating charities. Under the 2026 universal above-the-line deduction, the intent is to incentivize direct cash contributions to operating charities, and the policy design commonly excludes gifts to intermediaries like DAFs (as well as certain other vehicles) for this specific capped deduction.

If I donate $1,000 from my DAF to a nonprofit in 2026, do I get the $1,000 universal deduction?

In most cases, no — because the person making the “charitable contribution” for tax purposes is the DAF sponsor (the public charity), not you personally in 2026. You already received (or could have received) the charitable deduction when you contributed to the DAF in the year you funded it. A grant from the DAF to a nonprofit does not create a second charitable deduction for the original donor.

If you want a donor-first, practical walkthrough, see: What the New 2026 Charitable Tax Incentives Mean for You as a Donor.

How much you’ll save (and why this is a big deal)

Starting in 2026, charitable giving isn’t only “tax-deductible if you itemize.” For most Americans, it becomes a permanent pre-tax deduction.

Here’s the simple way to think about it:

- If you’re single, the tax code now effectively rewards your first $1,000 of giving each year with a pre-tax deduction.

- If you’re married filing jointly, it rewards your first $2,000 of giving each year.

That creates a clear “smart giving floor” for most people:

- Give at least $1,000 (individuals)

- Give at least $2,000 (married couples)

Your exact tax savings depends on your tax rate, but the concept is straightforward:

Pre-tax deduction × your tax rate = tax savings

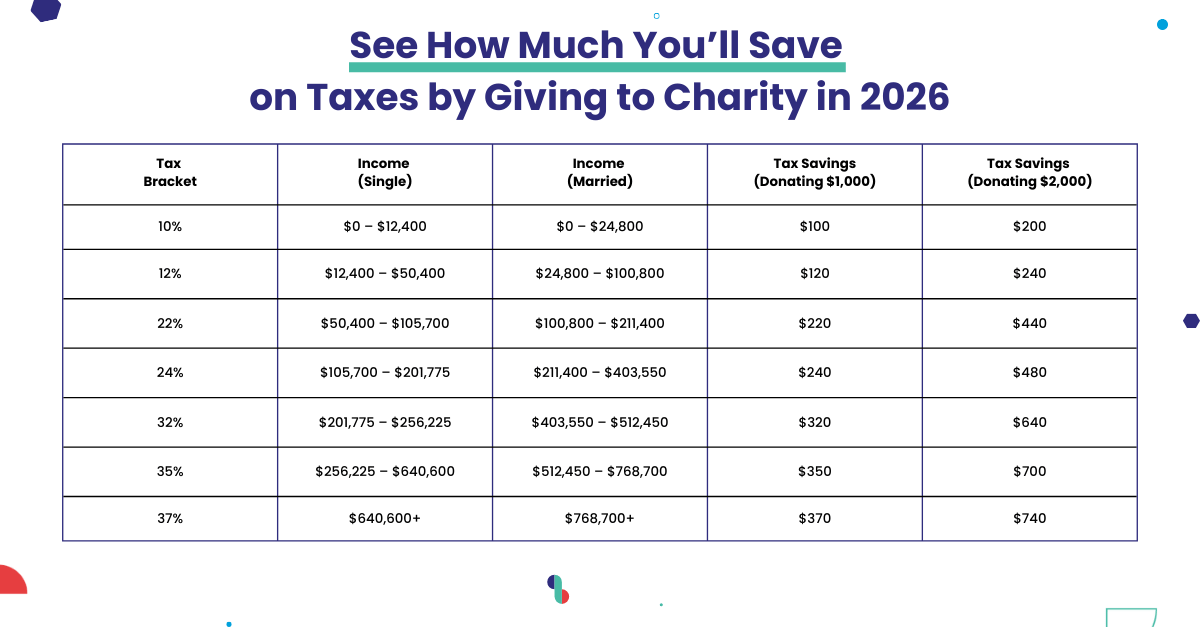

Example:If your tax rate is about 22% and you give $1,000, you save about $220 in federal taxes.If you’re married and give $2,000, you save about $440.

Here's a visual breakdown by tax bracket that you could reference and share:

For a deeper-dive on how much you could save from giving back in 2026 and beyond, check out this piece: See How Much You’ll Save on Taxes by Giving to Charity in 2026

Quick tax savings calculator (use your taxable income and a phone calculator)

You can estimate your savings in under a minute — no spreadsheets required.

Step 1: Pick your 2026 “smart giving” amount

- Single: use $1,000

- Married filing jointly: use $2,000

(If you gave less, use the amount you actually gave.)

Step 2: Find your federal tax bracket using your taxable incomeLook at your estimated taxable income (or last year’s taxable income as a proxy) and match it to the bracket in the table above. Use the rate for the bracket you fall into.

Step 3: Multiply

Use your phone calculator:

$1,000 (or $2,000) × your bracket rate = estimated federal tax savings

Examples:

- $1,000 × 12% = $120 saved

- $1,000 × 22% = $220 saved

- $2,000 × 24% = $480 saved

- $2,000 × 32% = $640 saved

That number is the approximate reduction in your federal tax bill attributable to this new pre-tax charitable deduction.

Tip: If you’re between brackets or unsure, this is still useful. The goal is not precision to the dollar — it’s making the incentive real and easy to understand.

Note: We made a fuller free tax savings calculator inside this blog on the new 2026 charitable tax incentives.

Documentation: what to keep and why it matters

Employees will not attach receipts to a return in most cases — but they should keep proof in case of audit.

This is exactly where systems help. Percent Pledge’s Giving Platform generates IRS-compliant donation receipts automatically and stores them in the employee dashboard. It also provides an annual giving summary so employees don’t have to dig through email at tax time.

If you’re an employee and want a checklist format, see: 2026 Charitable Giving Tax Incentives Checklist.

Deep Dive: What Employers Should Do in 2026

This section is written for HR, CSR, People leaders, and executives who own employee engagement programs.

Why the business case for social impact programs gets stronger in 2026

Employee giving and volunteering already support:

- engagement and retention

- employer brand

- recruiting

- culture

- community impact

The new tax incentives add something unusually practical: employees can now connect giving to personal financial benefit in a straightforward way. That makes it easier to promote giving without sounding like you’re pushing philanthropy for PR.

If you want three strong resources you can forward internally (especially to leadership), use:

- The Business Case for Corporate Social Responsibility in 2025

- 2025 Best Places to Work: Social Impact Benchmarking Report

- Employee Engagement Trends Report

These tax incentives aren’t the only driver — but they are the “extra push” that makes it easier to justify investment.

If you already have a workplace giving program

In 2026, the program you already have can work better — if you align design and communications to the new incentives.

What to review immediately

- Is it easy for employees to donate in recurring increments?

- Can employees quickly find eligible nonprofits?

- Does your program automate receipts and summaries?

- Does your matching cap encourage employees to reach the new threshold?

Platforms matter here because they reduce friction. Percent Pledge’s Giving Platform is designed to centralize giving, matching, and reporting so employees and admins don’t rely on manual processes.

If you do not have a workplace giving program

2026 is an unusually good time to launch, because:

- employees now have a clear reason to give

- programs are easier to communicate (“give up to $1,000/$2,000 and reduce your taxable income”)

- matching has a clearer strategic threshold

- giving platforms can launch quickly without heavy internal admin

A practical workplace giving overview is here: 2026 Charitable Giving Tax Rules: A Guide for Workplace Giving.

How to build or update programs optimized for 2026

1) Matching gifts (full subsection)

Matching becomes more strategic in 2026 because it complements the employee incentive.

The simplest concept:

- Employees are now incentivized to give (up to the cap)

- A match helps them feel their giving “goes further”

- Companies can design matching caps that nudge giving behavior

Many companies will evaluate whether their match cap should be at least $1,000 per employee, because that aligns with the new personal deduction threshold and creates a clean narrative.

Percent Pledge’s Matching Gifts automates matching without forms or manual approvals — which is the difference between “a match program on paper” and “a match program that actually gets used.”

For the step-by-step strategy guide, see: How to Update Matching Gift Programs for 2026.

2) Corporate grants (full subsection)

If your company funds grants, 2026 is a forcing function to get more structured:

- clearer eligibility

- predictable budgets

- better reporting

- easier finance reconciliation

This is where centralized grants management becomes important, especially when corporate giving is being evaluated against thresholds and documentation requirements.

3) Dollars for Doers / Cause Credits

Volunteer-based donation rewards help unify engagement and impact:

- Employees volunteer → company funds donations

- Those company-funded donations are trackable and reportable

- They become part of the overall corporate giving strategy

Percent Pledge supports volunteer rewards through flexible Cause Credits, and you can combine this with recognition using Impact Badges.

How employees actually execute giving in real life (and how employers can help)

Most employees don’t need a lecture. They need a simple path:

- “Here’s the amount that qualifies”

- “Here’s how to do it automatically”

- “Here are vetted options”

- “Here’s your receipt trail”

Percent Pledge helps employees give confidently in two key ways:

- Where to give

Employees can donate to specific nonprofits from a large verified database, or give by cause area using vetted portfolios. Verification is handled through charity vetting. - How to give the right amount

Recurring giving makes the threshold easy to hit (e.g., monthly donations that reach $1,000+ over a year).

If you want to help employees choose causes (and improve participation), the Passion Assessment makes employee interests visible, which helps CSR leaders plan smarter campaigns and communicate in a way that feels relevant.

For a full explanation of why platforms matter for execution, see: How Workplace Giving Platforms Help Employees Maximize the 2026 Charitable Deduction.

How to explain all of this to employees (without confusion)

Your comms should do three things:

- State the benefit clearly

- Explain the two caps ($1,000/$2,000)

- Tell them exactly what to do next (recurring giving is the simplest)

A comms-focused resource is here: How to Explain the New 2026 Donation Tax Incentives to Your Employees.

Mini FAQ for HR/CSR leaders (so this page stands alone)

Q: Can employees use this for 2025 donations when they file in 2026?

A: No — it applies to donations made in calendar year 2026 and beyond.

Q: Do employee donations through payroll deduction qualify?

A: Payroll giving is still the employee’s charitable donation. The key is whether it’s a gift to an eligible tax-deductible nonprofit.

Q: Does company matching increase the employee’s deduction?

A: No — the employee deduction is based on the employee’s own donation. Matching increases the total impact and may have corporate deductibility implications for the company.

Q: If employees donate to multiple nonprofits, does it still count?

A: Yes — what matters is the total amount of qualifying charitable giving during the year (up to the cap), and that the recipients are eligible.

For a longer Q&A reference you can forward internally, see: 2026 Charitable Giving FAQs: Employees, Employers & Nonprofits.

CFO and Finance Deep Dive

This section is written to be CFO-friendly, but still understandable for HR/CSR leaders who need to collaborate with Finance.

The corporate giving rules: the simple version

In 2026, corporate charitable deductions generally involve:

- a floor (below which deductions don’t apply), and

- a ceiling (above which deductions may be limited and carried forward)

If your company is a C-corp, Finance should treat charitable giving more like a planned line item than an ad hoc activity.

For the CFO overview post, see: What CFOs Need to Know About Corporate Giving in 2026.

Entity type: C-corp vs pass-through

C-corporations are directly subject to corporate deduction mechanics. Pass-through entities (LLCs taxed as partnerships or S-corps) handle deductions differently because income and deductions flow through to owners.

This is one reason HR/CSR leaders should avoid presenting the corporate giving rule as “one-size-fits-all” without a Finance check.

The 1% floor and 10% ceiling

Finance leaders will ask: “What portion of our giving is deductible this year?”

A clean mental model:

- If total giving is below the floor, it may be treated as nondeductible in the current year.

- If total giving exceeds the floor, deductions may apply to the band between floor and ceiling (subject to applicable rules).

- If giving exceeds the ceiling, carryforward rules may apply.

The practical implication is not “give more.” It’s “plan intentionally so you understand what you’re getting financially and why.”

Carryforward rules (why Finance cares)

Carryforward rules matter because they change how you time giving and how you communicate expectations internally. When rules introduce thresholds, “spread evenly across years” may not always be optimal.

This is where Finance teams may prefer:

- modeling taxable income early

- deciding whether to “bunch” contributions in certain years

- aligning grants, matching, and corporate giving into a single budget model

For a Finance collaboration guide, see: How to Talk About the 2026 Charitable Tax Changes With Your Finance Team.

Strategic implications for CFOs: decision framework (summarized here)

CFOs typically choose one of three strategies:

1) Engagement-first strategy (below threshold by choice)

Giving is treated as a culture, brand, and community investment. Taxes are not the objective.

2) Tax-aware strategy (structure giving to exceed thresholds)

Giving is budgeted and consolidated so the company understands its deductibility and documentation posture.

3) Hybrid strategy (employee engagement + structured company giving)

Matching and campaigns drive engagement while corporate grants ensure predictable impact and budget alignment.

We outline this in a crisp, forwardable format here: A CFO’s Decision Framework for Corporate Charitable Giving in 2026.

Budget modeling: what to actually do in Q4 and Q1

A practical Finance workflow looks like this:

- Forecast taxable income range (early estimate is fine)

- Decide whether corporate giving is intended to cross thresholds

- Determine which vehicles you’ll use (grants, matching, volunteer rewards, disaster relief, etc.)

- Centralize documentation and reporting for audit readiness

If your giving is fragmented across departments, you’re making this harder than it needs to be.

Why Platforms Matter More Than Ever

Incentives are only useful if employees can actually use them and employers can actually report them.

Platforms matter more in 2026 because they reduce three forms of risk:

1) Eligibility risk

Employees don’t want to guess whether an organization is eligible. Built-in verification through charity vetting helps prevent mistakes.

2) Documentation risk

Employees may need proof of donations if audited. Companies need clean reporting for Finance. A unified system helps generate receipts, store them, and produce annual summaries.

Percent Pledge’s Giving Platform provides IRS-compliant receipts and annual giving summaries automatically.

3) Operational risk

Manual matching forms, inconsistent records, and scattered donations increase administrative overhead and reduce participation. Automated Matching Gifts removes that friction.

How to Amplify Impact Across the Year

Tax incentives are one lever. Participation is another.

Most companies see the strongest engagement when they connect giving to moments people already care about:

- Giving Tuesday

- disaster response

- awareness and heritage months

- company milestones and culture events

Campaigns that drive participation

Percent Pledge supports campaign-style giving through Campaigns, including live reporting and leaderboards that make participation visible (which matters for engagement).

Disaster relief moments

Disaster response is one of the clearest moments where employees want to act fast. A structured approach helps ensure donations are eligible and receipted. See: Disaster Relief Donations.

Recognition that sustains engagement

Recognition drives repeat behavior. Tools like Impact Badges give employees visible credit and “hero treatment” that reinforces culture.

Planning resources

If you want a ready-made calendar and templates:

What Nonprofits Should Know in 2026

Nonprofits should expect two types of donor questions:

- “Does my donation qualify?”

- “How do I make this easy and trackable?”

Nonprofits that help donors answer those questions simply will win more recurring gifts.

Practical nonprofit actions

- Update donor messaging to mention the new $1,000/$2,000 above-the-line deduction

- Encourage recurring giving (“set it and forget it” is powerful)

- Strengthen workplace giving partnerships and matching visibility

- Ensure receipts and acknowledgments are timely and clear

For a nonprofit-focused version written specifically for fundraising teams, see: 2026 Charitable Giving Tax Rules: What Nonprofits Should Know.

Condensed FAQs (Quick Answers)

Can I use this for donations I made in 2025 when I file taxes in 2026?

No. This applies to donations made in 2026 and later.

Do donations made through workplace giving count?

Yes — if they are the employee’s donations to eligible tax-deductible nonprofits.

Does matching count for the employee deduction?

No. Matching is a separate company donation. It increases impact and has employer-side implications, but it does not increase the employee’s personal cap.

Do I need receipts?

You should keep proof in case of audit. Platforms can automate this.

For a longer, copy-paste-ready reference: 2026 Charitable Giving FAQs.

How All of This Fits Together

The 2026 changes align incentives across the system:

- Employees can give and see a straightforward tax benefit

- Employers can design programs that increase participation and make giving easier

- Finance teams can budget and document giving more predictably

- Nonprofits can encourage recurring, eligible, trackable donations

This is one of those rare moments where doing good and doing the practical thing can align — as long as you make it easy.

That’s exactly what workplace giving infrastructure is for.

Clear Next Step

If you want help making these changes real inside your organization — updating matching, improving participation, simplifying giving, and producing clean reporting for Finance — we can help.

Book time with our team: Schedule a meeting

.png)